Global economy on firmer ground, but with divergent recoveries amid high uncertainty

Global prospects remain highly uncertain one year into the pandemic. New virus mutations and the accumulating human toll raise concerns, even as growing vaccine coverage lifts sentiment. Economic recoveries are diverging across countries and sectors, reflecting variation in pandemic-induced disruptions and the extent of policy support. The outlook depends not just on the outcome of the battle between the virus and vaccines—it also hinges on how effectively economic policies deployed under high uncertainty can limit lasting damage from this unprecedented crisis.

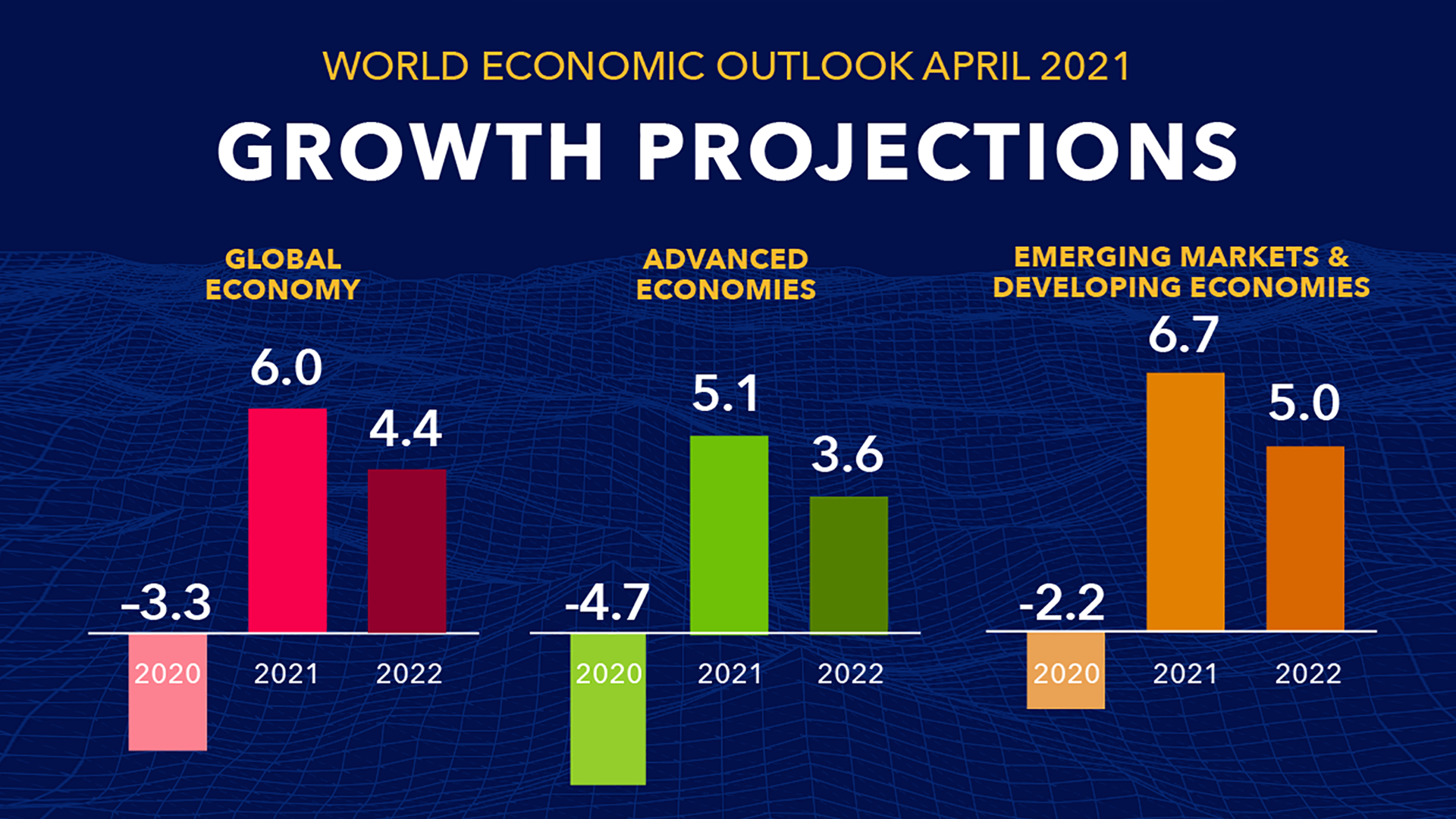

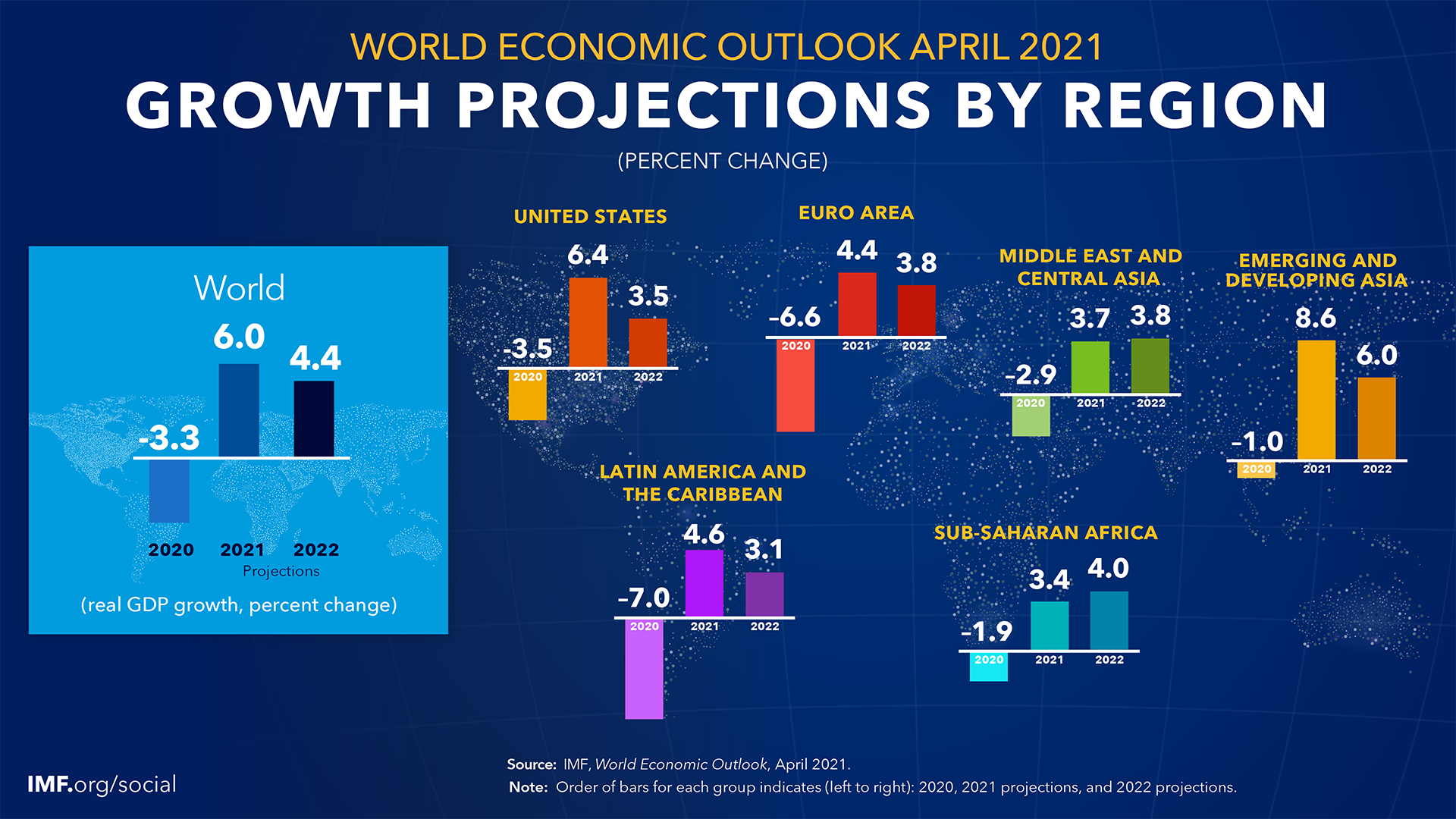

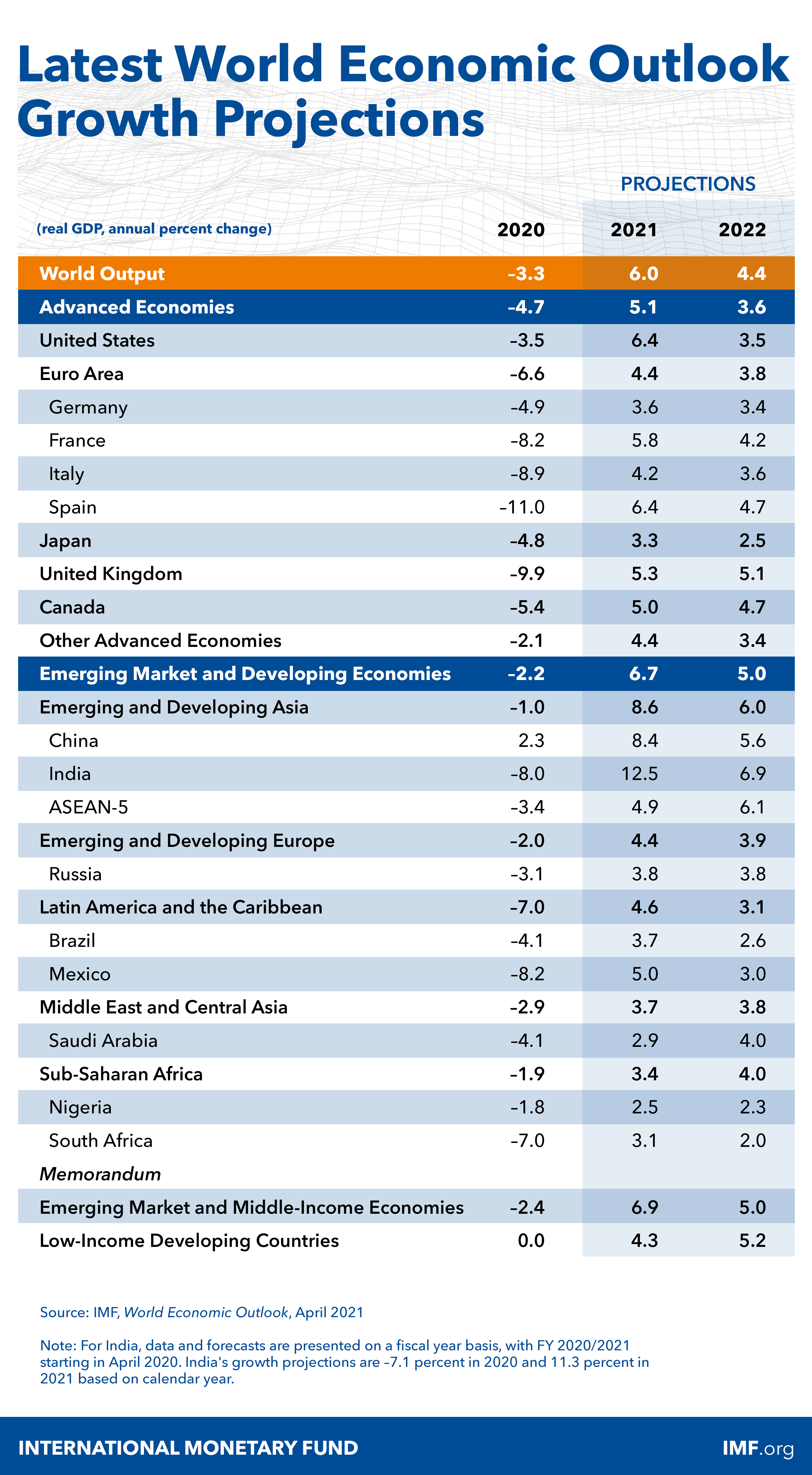

Global growth is projected at 6 percent in 2021, moderating to 4.4 percent in 2022. The projections for 2021 and 2022 are stronger than in the October 2020 WEO. The upward revision reflects additional fiscal support in a few large economies, the anticipated vaccine-powered recovery in the second half of 2021, and continued adaptation of economic activity to subdued mobility. High uncertainty surrounds this outlook, related to the path of the pandemic, the effectiveness of policy support to provide a bridge to vaccine-powered normalization, and the evolution of financial conditions.

Global Prospects and Policies

Although the contraction of activity in 2020 was unprecedented in living memory, extraordinary policy support prevented even worse economic outcomes. One year into the COVID-19 pandemic, a way out of this health and economic crisis is increasingly visible, but prospects remain highly uncertain. The strength of the recovery will depend in no small measure on a rapid rollout of effective vaccines worldwide. Much remains to be done to beat back the pandemic and avoid persistent increases in inequality within countries and divergence in income per capita across economies.

After-Effects of the COVID-19 Pandemic: Prospects for Medium-Term Economic Damage

This chapter examines the possible persistent damage (scarring) that may occur from the COVID-19 recession and the channels through which they may occur. Importantly, financial instabilities—typically associated with worse scarring—have been largely avoided in the current crisis so far. While medium-term losses are expected to be lower than after the global financial crisis, they are still substantial, at about 3 percent lower than pre-pandemic anticipated output for the world in 2024. The degree of expected scarring varies across countries, depending on the structure of economies and the size of the policy response. Emerging market and developing economies are expected to suffer more scarring than advanced economies.

Recessions and Recoveries in Labor Markets: Patterns, Policies, and Responses to the COVID-19 Shock

The labor market fallout from the COVID-19 pandemic shock continues, with young and lower-skilled workers particularly hard-hit. Preexisting employment trends favoring a shift away from jobs that are more vulnerable to automation are accelerating. Policy support for job retention is extremely powerful at reducing scarring and mitigating the unequal impacts from the acute pandemic shock. As the pandemic subsides and the recovery normalizes, a switch toward worker reallocation support measures could help reduce unemployment more quickly and ease the adjustment to the permanent effects of the COVID-19 shock on the labor market.

Shifting Gears: Monetary Policy Spillovers During the Recovery from COVID-19

Monetary policy easing by advanced economies early in the pandemic provided much financial relief to emerging markets. Looking ahead, a multispeed recovery from the crisis will raise challenges. Our analysis suggests that while a US tightening resulting from a stronger US economy tends to be benign for most emerging market economies, a surprise tightening triggers capital outflows from emerging markets. It will thus be important for advanced economies to explain clearly how they will implement their monetary policies during the recovery. The chapter’s analysis also suggests that emerging market economies can reduce their vulnerability to adverse financial spillovers by adopting more transparent and rules-based monetary and fiscal frameworks.

Publications

-

June 2024

Finance & Development

- An IMF for Tomorrow

-

September 2023

Annual Report

- Committed to Collaboration

-

Regional Economic Outlooks

- Latest Issues