Global debt remained above pre-pandemic levels in 2021 even after posting the steepest decline in 70 years, underscoring the challenges for policymakers.

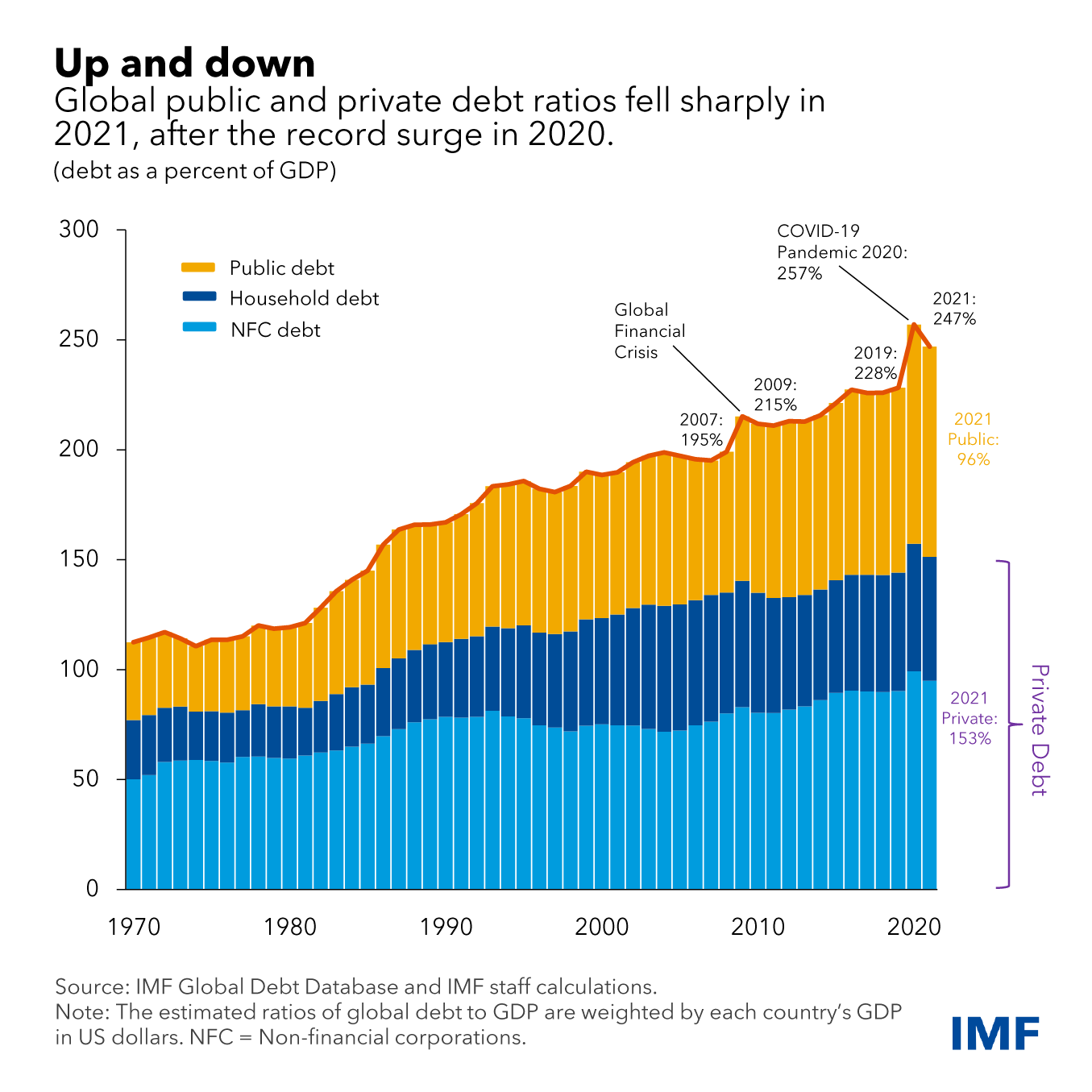

Total public and private debt decreased in 2021 to the equivalent of 247 percent of global gross domestic product, falling by 10 percentage points from its peak level in 2020, according to the latest update of the IMF’s Global Debt Database. Expressed in dollar terms, however, global debt continued to rise, although at a much slower rate, reaching a record $235 trillion last year.

Private debt, which includes non-financial corporate and household obligations, drove the overall reduction, decreasing by 6 percentage points to 153 percent of GDP, according to our unique tally, which has been published annually since 2016. The decline of 4 percentage points for public debt, to 96 percent of GDP, was the largest such drop in decades, our database shows (for further details see the 2022 Global Debt Monitor).

The unusually large swings in debt ratios are caused by the economic rebound from COVID-19 and the swift rise in inflation that has followed. Nevertheless, global debt remained nearly 19 percent of GDP above pre-pandemic levels at the end of 2021, posing challenges for policymakers all over the world.

Variation across countries

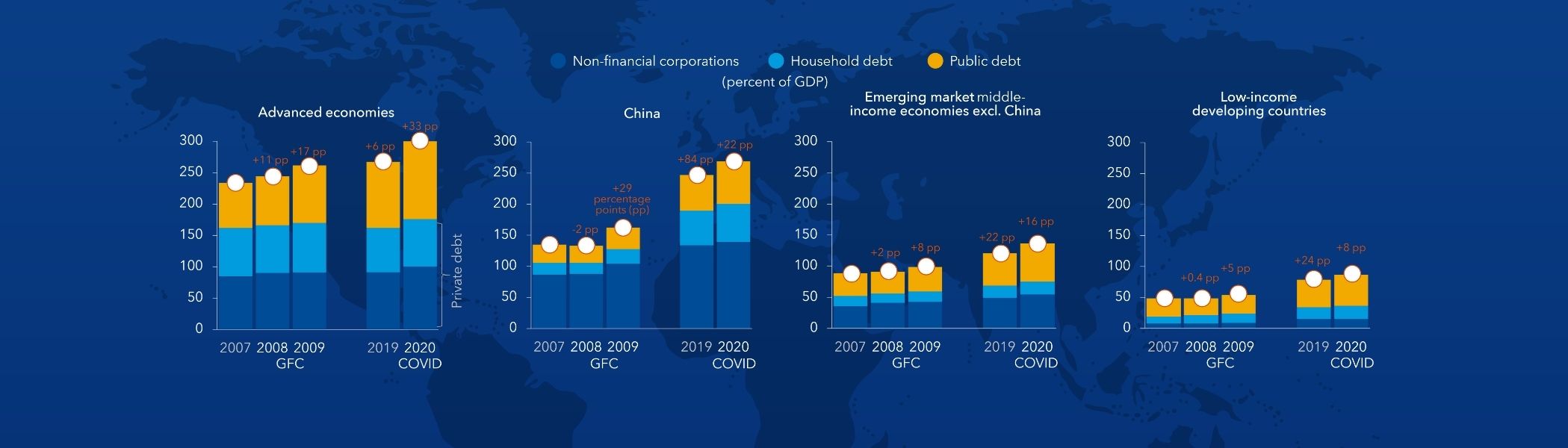

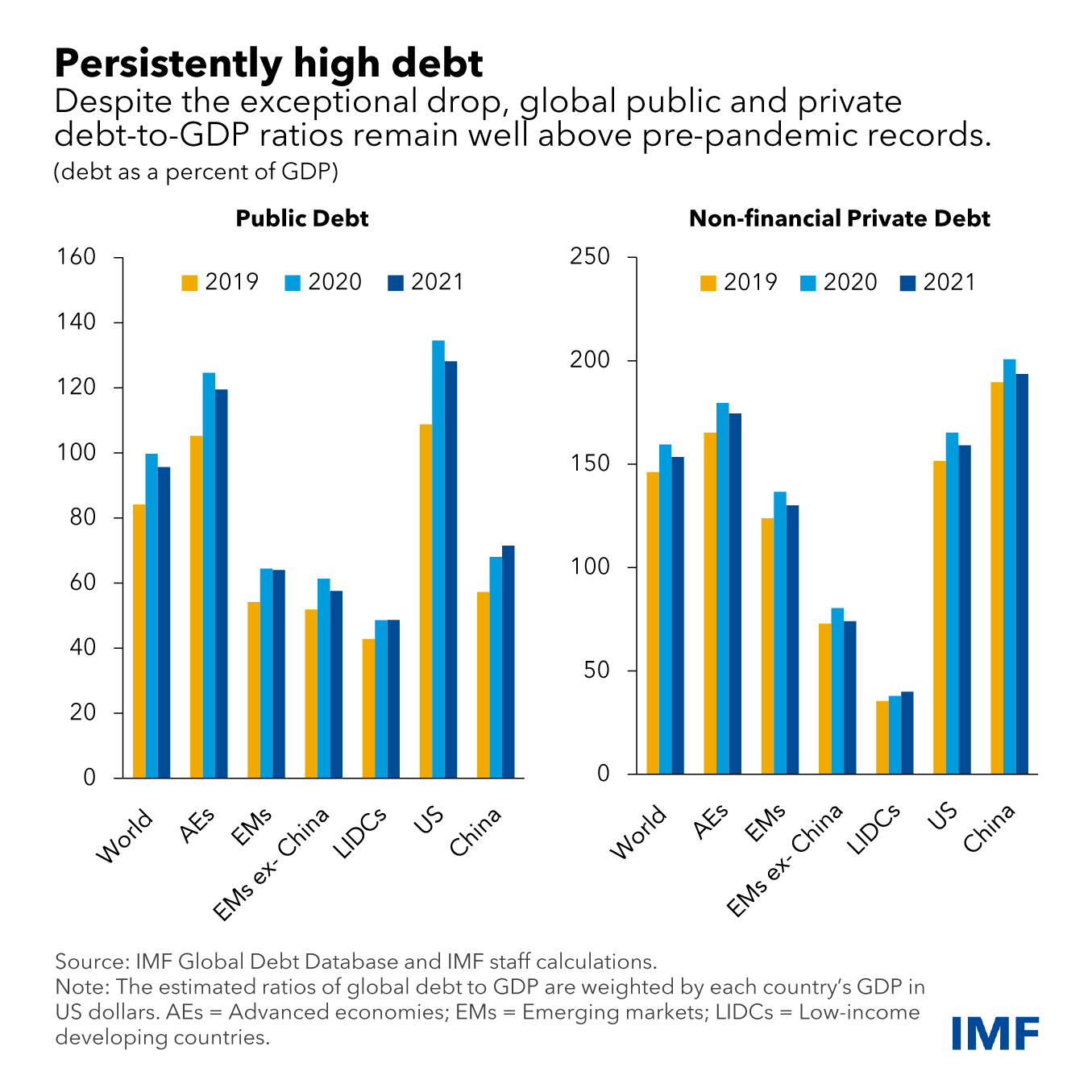

Debt dynamics varied significantly across country groups, however.

The fall in debt was largest in advanced economies, where both private and public debt fell by 5 percent of GDP in 2021, reversing almost one-third of the surge recorded in 2020.

In emerging markets (excluding China), the fall in debt ratios in 2021 was equivalent to almost 60 percent of the 2020 increase, with private debt falling more than public debt.

In low-income developing countries, total debt ratios continued to increase in 2021, driven by higher private debt.

Factors behind the global debt swings

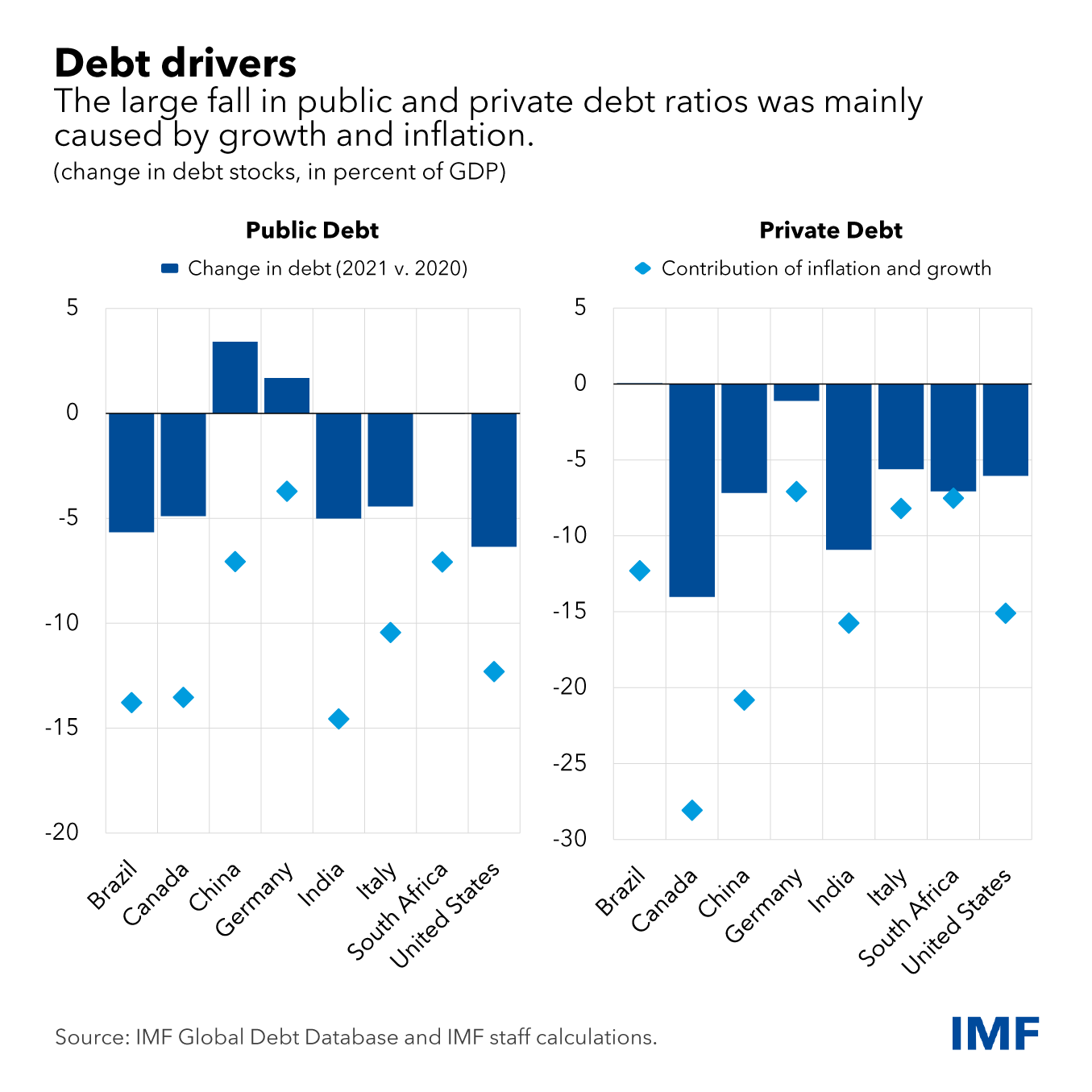

Three main drivers explain these unusually large movements in both private and public debt around the world:

-

Large fluctuations in economic growth. The economic recession at the onset of the pandemic contributed to a

pronounced drop in GDP, which was reflected in the sharp rise in

debt-to-GDP ratios in 2020. As economies moved on from the worst of the

pandemic, the strong rebound in GDP helped the 2021 fall in debt

ratios.

-

High and more volatile inflation.

Likewise, inflation rates fell significantly in the first year of the

pandemic. This trend was reversed in 2021 as prices rose sharply in

many countries. During 2020 and 2021, economic activity and inflation

moved together: inflation fell and then rose with output. These factors

induced large swings in nominal GDP that contributed to the changes in

debt ratios.

- Effects of economic shocks on the budgets of governments, firms, and households. The volatile economic conditions also had a considerable impact on debt dynamics through budgets. Debt and deficits increased significantly in 2020 because of the economic recession and the sizable support extended to individuals and businesses. In 2021, fiscal deficits declined but remained above their pre-pandemic levels (see October 2022 Fiscal Monitor).

A few country examples illustrate these effects. The economic rebound and rise in inflation pushed debt down by more than 10 percentage points of GDP in Brazil, Canada, India, and the United States, but actual debt fell less owing to the financing needs of government and the private sector. In other cases—for example, in China and Germany—public debt increased as the large deficits more than compensated for the rise in nominal GDP.

More generally, the rebound helped to reduce public debt ratios between 2 and 3.5 percent of GDP (with the largest effect among advanced economies), while inflation shaved off between 1.5 and 3 percentage points (the effect was more pronounced in emerging markets). Conversely, fiscal deficits increased public debt by around 4.5 percent of GDP with considerable variation across countries.

How governments should respond

Managing the high debt levels will become increasingly difficult if the economic outlook continues to deteriorate and borrowings costs rise further. The high inflation levels continue to help reduce debt ratios in 2022, especially where deficits are returning to pre-pandemic levels.

However, the relief to debt dynamics from “inflation surprises”—that is, when price levels are different from what was expected—and the temporary growth rebound cannot be permanent (see April 2022 Fiscal Monitor). If high inflation were to become persistent, spending will increase (for example, on wages) and investors will demand a higher inflation premium to lend to governments and private sector.

The weaker growth outlook and tighter monetary policy calls for prudence in managing debt and conducting fiscal policy. Recent developments in bond markets show investors’ heightened sensitivity to deteriorating macroeconomic fundamentals and limited fiscal buffers.

Governments should adopt fiscal strategies that help reduce inflationary pressures now and debt vulnerabilities over the medium term, including by containing expenditure growth—while protecting priority areas, including support to those hardest hit by the cost-of-living crisis. This would also facilitate the work of central banks and allow for smaller increases in interest rates than would otherwise be the case. In times of turbulence and turmoil, confidence in long-run stability is a precious asset.

—This blog incorporates research by Youssouf Kiendrebeogo, Virat Singh, Zhonghao Wei, Andrew Womer, and Chenlu Zhang.