A funding squeeze has hit the region hard

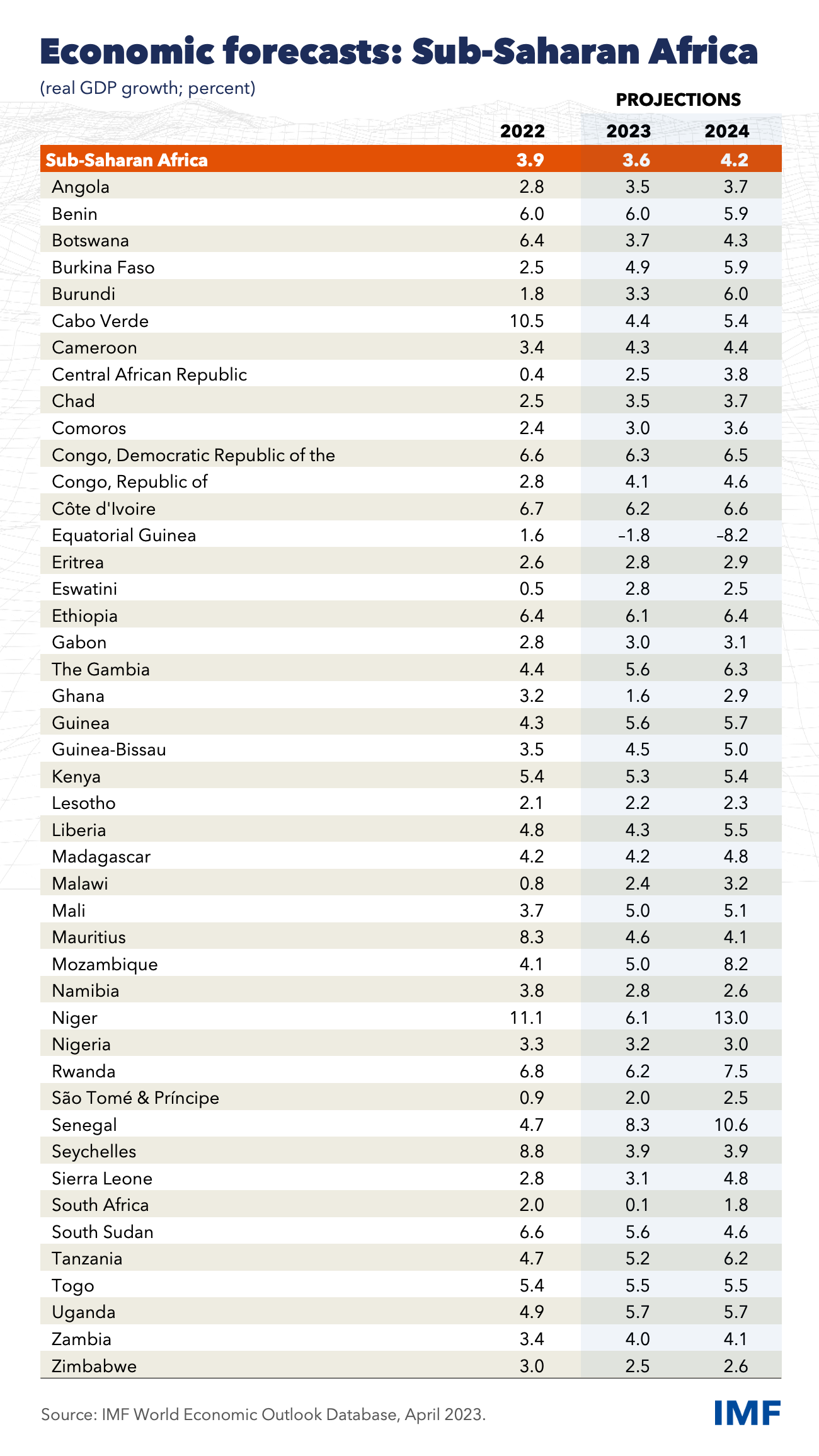

Persistent global inflation and tighter monetary policies have led to higher borrowing costs for sub-Saharan African countries and have placed greater pressure on exchange rates. Indeed, no country has been able to issue a Eurobond since spring 2022. The interest burden on public debt is rising, owing to a greater reliance on expensive market-based funding combined with a long-term decline in aid budgets. The lack of financing affects a region that is already struggling with elevated macroeconomic imbalances. Public debt and inflation are at levels not seen in decades, with double-digit inflation present in about half of the countries—eroding household purchasing power and striking at the most vulnerable. In this context, the economic recovery has been interrupted. Growth in sub-Saharan Africa will decline to 3.6 percent this year. Amid a global slowdown, activity is expected to decelerate for a second year in a row. Still, this headline figure masks significant variation across the region. The funding squeeze will also impact the region’s longer-term outlook. A shortage of funding may force countries to reduce resources for critical development sectors like health, education, and infrastructure, weakening the region’s growth potential.

Geoeconomic Fragmentation: Sub-Saharan Africa Caught between the Fault Lines

Over the past two decades, sub-Saharan Africa has forged economic and trade alliances with new economic partners. While the region has benefited from increased global integration during this period, the emergence of geoeconomic fragmentation has exposed potential downsides. Sub-Saharan Africa stands to lose the most in a severely fragmented world compared to other regions, but there could also be potential benefits if fragmentation is limited. It is important for countries to build resilience against likely fallouts from fragmentation and position themselves to benefit from possible changes in trade and capital flow patterns.

Managing Exchange Rate Pressures in Sub-Saharan Africa—Adapting to New Realities

Sub-Saharan African countries, as elsewhere, have recently faced significant exchange rate pressures driven predominantly by external factors, including tighter financing conditions and adverse terms of trade which are expected to be durable. Currency depreciations have contributed to higher inflation and public debt and deteriorated the trade balance in the near term. However, with reserves running low, most non-pegged countries have no choice but to let the exchange rate adjust and tighten monetary policy to mitigate the impact on inflation. To preserve external stability, pegged countries are bound to adjust monetary policy in line with the country of the peg. In both country groups, fiscal consolidation can help to rein in external imbalances and contain the increase in debt related to currency depreciation.

Closing the Gap: Concessional Climate Finance and Sub-Saharan Africa

Although sub-Saharan Africa is the world’s smallest contributor to global greenhouse gas emissions, it is the most vulnerable to climate-related shocks. Addressing climate change will be costly, and few sub-Saharan African countries have the resources or fiscal space to tackle this challenge without assistance from the international community. Concessional finance should be scaled up to strengthen the region’s resilience to climate change and to help speed the green energy transition. This note explores some available options, highlighting the untapped resources currently available from multilateral climate funds, and noting in particular the demand for new ways of connecting public, private, and concessional finance to lift investment and close the gap between resources and needs. Part of the effort to scale up climate finance will entail steps to address exiting bottlenecks—including on the part of recipient countries—in order to ensure that committed funds are used swiftly and effectively.

Publications

-

June 2024

Finance & Development

- An IMF for Tomorrow

-

September 2023

Annual Report

- Committed to Collaboration

-

Regional Economic Outlooks

- Latest Issues